Building envelope adhesives and sealants market forecast at $5.9 billion by 2026

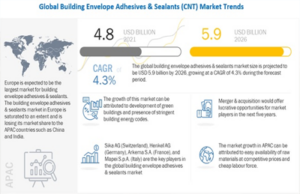

Pune, India – The market size for building envelope adhesives and sealants is projected to grow from $4.8 billion in 2021 to $5.9 billion by 2026, at a CAGR of 4.3 percent between 2021 and 2026, according to MarketsandMarkets. The market growth of building envelope adhesives and sealants in the APAC region is due to easy availability of raw materials at competitive prices and a cheap labor force.

COVID-19 has made a significant economic impact on various financial as well as industrial sectors, such as travel and tourism, manufacturing and aviation. The worst economic recession is expected during 2020-2021, according to World Bank and IMF. With the increasing number of countries imposing and extending lockdowns, economic activities are declining, impacting the global economy.

In the recent past, the global economy became substantially more interconnected. The adverse consequences of various steps related to the containment of COVID-19 are evident from global supply chain disruptions, weaker demand for imported products and services, and an increase in the unemployment rate. Risk aversion has increased in the financial market, with all-time low interest rates and sharp declines in equity and commodity prices. Consumer and business confidence have also reduced significantly.

The increasing penetration of sealants in new applications, such as ductwork, anchoring application and structural glazing in the construction industry is driving the building envelope adhesives and sealants market. The major applications of construction sealants are in window framing, sanitary and kitchen, expansion joints, floor systems, walls and panels. Under changing atmospheric conditions, they provide stress-bearing capability and prevent from cracking.

Adhesives are used in various applications such as carpet laying, tile installation and exterior insulation systems in the construction industry. These applications have spurred the growth of the building envelope adhesives and sealants market.

Europe and North America are strictly regulated by environmental laws regarding the production of chemical and petro-based products. Agencies such as Epoxy Resin Committee (ERC), European Commission (EC) and other regulatory bodies are governing the manufacturing of solvent based products in these regions. These regulations are restraining the growth of the construction adhesives market. The companies are not able to shift their entire focus on manufacturing green and environmentally-friendly products, which are also hampering their business revenue.

The rising trend of using environmentally-friendly or green products in various applications is driving the demand for green adhesives or those with low VOCs. Stringent regulations implemented by USEPA (United States Environmental Protection Agency), Europe’s REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), Leadership in Energy and Environmental Design (LEED) and other regional regulatory authorities have forced the manufacturers to produce environmentally friendly adhesives with low VOC levels. The shift toward a more sustainable product portfolio has provided the industry a significant growth opportunity.

The major players manufacture environmentally-friendly construction adhesives. These green adhesive solutions are made from renewable, recycled, remanufactured or biodegradable materials; the use of these environmentally-friendly products also benefits the health of the occupants

There is a lack of awareness among the consumers, as well as building professionals about building envelopes. The biggest gap between today’s regulations and recommended energy performance are found in southern Europe. There needs to be a major initiative in this region to raise awareness and bring building regulations.

In some cases, buildings are not even insulated to code, as per the location, weather conditions and structure of the building; and this happens not necessarily due to design but because of lack of awareness on the part of some architects and building code officials. This has resulted in a lack of proper insulation in many commercial buildings in comparison to what it should be.

The market for polyurethane adhesive resin is driven by its demand in various applications such as façade panel fixing, flooring, roofing, sanitary sealing and wall joints. These adhesives are formulated by liquid reactive (two part), hot melt and low-VOC technologies. The key players such as HB Fuller, 3M, and ICP Group are the main producers of polyurethane-based adhesives.

Treatment of building with thermal insulation solutions like building envelope may help in reducing energy consumption. For APAC and the Middle East and Africa, roofing is the major contributor of heat gain in buildings. Various studies are available to determine heat flow through different building components. High temperature in summer ranging from 104-122°F in this region necessitate cooling of buildings to provide a comfortable and workable living environment indoors. For non-conditioned residential and other types of buildings, peak temperature is managed by using roof insulation. The use of thermal insulation to minimize solar heat gain in summer and heat loss in winter through roof is expected to drive the growth of roof insulations, and thus the building envelope adhesives and sealants market.

APAC is increasingly becoming an important trade and commerce center. The region is currently the fastest-growing and the largest market for building envelope adhesives and sealants. The manufacturers of building envelope adhesives and sealants are targeting this region as it has the largest construction industry, accounting for approximately 40 percent of the construction spending, according to the World Bank. Easy availability of raw materials at competitive prices and cheap labor force have made APAC the biggest market for construction products. Global manufacturers are increasingly setting up their production plants in the region in a bid to ramp up production and increase sales.

The spread of COVID-19 started in China in early January 2020. Within a small period, the virus spread to other Asian countries, such as Japan, India, South Korea and Thailand, resulting in a rapidly increasing number of positive cases and deaths. The pandemic situation led national governments across APAC to announce lockdowns, leading to a decrease in traffic and temporary closure of construction and mining activities, manufacturing industries, and others. Since China is a global manufacturing hub, it was significantly impacted by the COVID-19 pandemic; this in turn had an adverse effect on the building envelope adhesives and sealants market in APAC in 2020.

The key players operating in the market are Sika AG (Switzerland), Henkel AG (Germany), Arkema S.A. (France), Mapei S.p.A. (Italy), The 3M Company (U.S.), ICP Group (U.S.), H.B. Fuller Company (U.S.), The Dow Chemical Company (U.S.), tremco illbruck GmbH (Germany) and Soudal Group (Belgium).